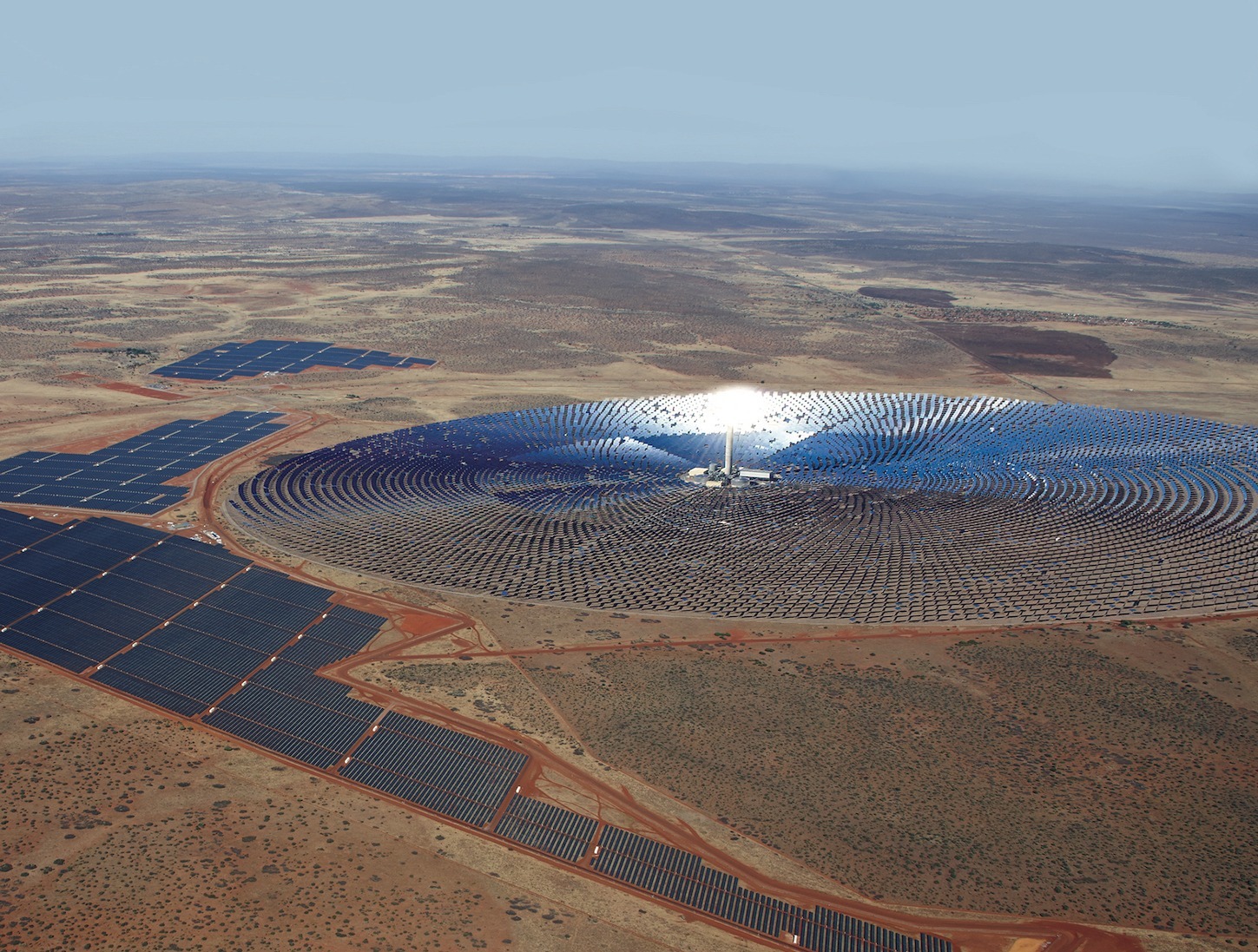

SolarReserve / ACWA Power Redstone 100 MW Power Tower CSP IMAGE@SolarReserve

SolarPACES interviewed Bernard Geldenhuys, the Senior Transactor in the Power and Infrastructure team at Investec Bank, a lender with 8,300 employees that has been closely involved in the 100 MW Redstone solar power tower since 2018, when its delayed PPA was signed with Eskom, as the first commercial bank to support the transaction, providing senior debt worth R750m and foreign exchange and interest rate hedging. Redstone is now financed at R11.5bn (about $837 million USD) and is finally about to break ground, with completion planned by the end of 2023. Eskom had put it on hold in 2016 along with other renewable PPAs. Thanks to the benefits of scale and ongoing reductions in CSP components, Investec claims that Redstone will have the “lowest tariff” of South Africa’s Concentrated Solar Power (CSP) plants but did not reveal the price of the 20-year PPA with Eskom.

Q: How were you able to get the Redstone tower CSP back on track?

A: Redstone is important for the South African economy. Eskom urgently requires approximately 6,000 MW of base load power over the next five years. This is being partly addressed by the 2,000 MW RMIPPP Programme. ACWA Power Redstone, with its 33-month construction period, 12 hours of thermal energy storage and 35-year useful life, is capable of providing fully dispatchable baseload electricity to the grid in support of these requirements. It’s the first Renewable Energy Independent Power Producer Procurement (REIPPP) project to provide ancillary services such as grid stabilisation, to Eskom, at no additional cost.

Q: Do you put together financial consortiums with other lenders to get renewables built?

A: Yes, Investec has been the arranger on multiple renewable energy projects, including the 94 MW Aurora WindPower project, the 50 MW ACWA Power Bokpoort CSP project, 100 MW Kathu Solar Park project and the 75 MW Sishen Solar project.

Q: Redstone was originally developed by SolarReserve. Did ACWA Power switch to any new component suppliers and if so, did that help make it more bankable?

A: Post the exit of SolarReserve the main equipment suppliers were changed to Brightsource Energy for heliostats and their control systems, and CMI for the central receiver. To our knowledge this change did not require a change in permitting for the project. The PPA amendment did not depend on the technology provider. The track record of ACWA Power, Brightsource and CMI contributed to the bankability of the project.

(CMI – now John Cockerill– was also selected for the receiver on ACWA Power’s DEWA project.)

Q: Are these delays in accepting renewable PPAs a problem going forward there?

A: Although the procurement of BW4 was substantially delayed, I think we are on the right trajectory. In March 2021, the DMRE announced the opening of Bid Window 5 of the REIPPP Programme which will procure 2,600MW of renewable energy from IPPs. The announcement of Bid Window 6 is expected to occur during the course of 2021. This aggressive roll-out is aligned with the IRP 2019 under which 6,000 MW of new solar PV capacity and 14,400 MW of new wind power capacity is to be commissioned by 2030. Last month the DMRE released a notice in the government gazette of its intent to raise the threshold for embedded generation from 1MW to 10MW. This will bolster the roll-out of renewable energy (predominantly rooftop solar) in the commercial and industrial space. Also, interesting that a large component of the projects that received Preferred Bidder status for the RMIPPP Programme have a renewable element to it.

Q: What regulations drive South African renewables?

A: The South Africa government is a signatory to the COP 21 agreement and intends to make the country carbon neutral by 2050. SA will develop its own renewable energy projects for at least the next 10 years to come, because of the economic benefits it provides in terms of infrastructure build, jobs, etc. DMRE must commit to their ambitions under the IRP 2019 – which does seem to be the case.

Q: Given your breakthrough on Redstone, and the excellent performance of Bokpoort, are you working with ACWA Power on any new CSP for South Africa?

A: Not currently. There is no allocation for CSP in the current Bid Window 5 of the Department of Mineral Resources and Energy (DMRE)’s Renewable Energy Independent Power Producer Procurement (“REIPPP”) Programme.

CSP was also not a viable option for the recent Risk Mitigation Independent Power Producer Procurement (“RMIPPP”) given the short construction period because of the longer lead times required for a CSP plant.

Q: Didn’t one of the first South African CSP plants try steam for thermal energy storage?

A: Only a tower project; Khi. All trough CSP in South Africa have molten salt storage systems and so will Redstone. Khi was Abengoa’s pilot plant at 50 MW scale, following their PS10 and PS20 projects in Spain, before a first full scale tower CSP at 100 to 150 MW. Some issues with steam affect overall plant efficiency. The thermodynamics of a smooth continuous steam generation process where the steam is generated in the tower is very complex and fraught with lots of issues. It is extremely challenging to maintain the overall steam quality from the receiver, where it is produced, down into the steam storage system and on to the steam turbine. Steam storage accumulators are large, expensive and at best have only a few hours of storage capacity. Much more heat can be stored in molten salt, and for longer periods.

Q: ACWA Power’s other CSP in South Africa, the 50 MW Bokpoort trough plant you financed seems to be performing well. You led a refinancing round at 5 billion rand – about $366 million in USD. Is it repaying loans on time?

A: Yes, Bokpoort is performing in line with expectations.

Q: Though there were a lot of PV firms building big solar farms in the US, only one (First Solar) wound up getting nearly all the big solar farm contracts: is ACWA becoming the CSP equivalent?

A: I think so, yes. ACWA Power currently has about 1,510 MW of CSP projects in its portfolio, with Redstone bringing this to 1,610 MW. ACWA Power seems to be increasingly the one developer with new projects: Morocco, Dubai, and now Redstone is back in South Africa.

Q: Are you involved in the Biden MoU with Botswana and Namibia for 5 GW of solar?

A: No, we are not yet involved. We have only read about it, but we are not sure what exactly is planned and who will be the off-taker for so much power. The only reasonable chance of this succeeding is if the project intends to make green hydrogen and export this as fuel.

Q: Didn’t Botswana and Namibia do some CSP feasibility studies? Did they decide to go ahead?

A: No. All Namibian and Botswana CSP projects have been shelved and, in both countries, solar PV plus battery storage in selected projects is being planned. I am not aware that a single CSP plant is still being developed. Both countries consume relatively small amounts of electricity and building large 150 MW CSP plants would represent about 25% of total electricity demand. Since both countries are sparsely populated and cover a large land area, it makes more sense to build small solar PV plants plus storage closer to consumers.

Q: Aren’t there any regional power markets?

A: Currently power can only be traded bi-laterally between the various countries state owned power utilities in Southern Africa. There is no regional power market into which the 5000 MW can be sold. This could take at least another 5 to 10 years to sort out the politics to achieve a regional market.

Q: As independent financial advisor in energy projects there: have you advised on desalination or hydrogen production where CSP and CST might come in?

A: A 5,000 MW solar project jointly developed by these two countries with hydrogen/ammonia production near a Namibian harbor with an expert anchor client might be the solution to achieve multiple objectives; desalinated water, cheap electricity for both countries, export earnings for Namibia/Botswana. Similar projects are currently planned in Australia. If large scale green hydrogen/ammonia production is pursued, then desalination of water is required for the electrolysis of the water to obtain hydrogen. Since the water consumption for hydrogen production consumes the bulk of the water, the added cost for desalinated water is relatively low. Many studies have been done where waste heat from thermal plants is used to assist with desalination. Ultimately the cost of electricity will determine the technology to be used. Electricity costs from large scale solar PV plants are currently being offered at prices of well below US$ 0,03/kWh and in some cases below US$0.02/kWh, where the lowest cost of electricity from CSP plants is around US$0.07/kWh in the UAE.

Q: How fast do you see commercializing hybrid thermal storage – or SCO2 CSP? Or do you see additional CSP in the region using current technology?

A: Unlikely. Maybe in Morocco there might be more projects. As you know there is the intent to hybridize CSP with solar PV technology in the latest projects in Morocco; Midelt. We will need to see what costs they come in at.

There are also technology projects to replace the steam-based power Rankine cycle with a super-critical CO2 based Brayton cycle to increase overall plant efficiencies and reduce plant complexities. But all these attempts will require at least another 10 years to mature the technologies. The most important cost reduction factor has been the production capacity scaling we have seen for solar PV. CSP plants will always remain discrete single projects, and although the designs can be standardized they remain complex to build and operate.

Q: Any thoughts on the future of energy globally?

A: I see no future in coal-based investments. Limited future for the next 20 years in gas-based power plants – only to help create a bridge into a zero-carbon future. Solar PV and wind power, onshore & offshore. More investment into storage technologies, especially long-term storage over 8 hours. Also, more investments into energy efficiency and to make hydrogen an important future energy carrier to decarbonize many of the industries where heating and cooling dominates. So far, the infrastructure roll out is too slow to meet the 1.5 C target, since it is generally not recognized that electricity is only a small part of the total energy picture.